Futarchy - The Future of Governance

Experimenting with Market Wisdom in Decentralized Ecosystem

Around 5000 years ago, civilizations came into existence. Smaller cities turned into large governed areas. Administrations with different kinds of governance forms were developed to represent a civilization, then cities, states and now countries. Till date we have 13 forms of government (democratic, non-democratic & other). In fact, Gagnon (2018) identifies around 2,234 different forms of democracy alone. All but to serve towards the national welfare in any means possible. The question therefore, stands: After centuries of squabbling over which form, works best for people, do we need any more debates? Isn’t that similar to starting from scratch? Everything seems fine now, what are the problems with current forms of government? Do we really need a change? Well, change is inevitable!

This century has a unique opportunity to work with Web 3.0 — the Blockchain revolution and become pioneers. We can experiment, implement, analyse and reward ourselves, all within this era, using the best of our ideas. One such idea that has come to surface after 24 years, is ‘Futarchy’ and it is now possible to challenge the conventional wisdom.

“It's a question in government. It's a question in business. It’s a very fundamental, difficult problem. I think there's potential for doing a lot better than we've done.”

- Robin Hansen, CSPI Podcast

The term ‘Futarchy’ was coined by Robin Hansen, an Economist and Professor at George Mason University, who published this idea in 2007 (first working paper in 2000). Futarchy, according to the author of “Shall We Vote on Values, But Bet on Beliefs?”, is a form of government which uses the successes of speculative markets as information aggregation mechanisms to help reduce the failures of democracies. Democracy is as close as you can get with counting people’s opinion on subjects of matter. Futarchy can be considered as a new form of democracy but more improved and egalitarian. In this article, we are all talk about Futarchy, a market based governance system! The Meta-DAO, a decentralized autonomous organisation, has taken upon itself to be the preacher for this idea, building a market that will be self-sufficient. I know it sounds exciting, but, we will wait for it until the mid of this article. This article will answer reader’s question on:

✔ Why do we need new governance model?

✔ What is the idea behind this new governance model - Futarchy?

✔ How does Futarchy work? And what can be the possible problems?

✔ Why is Futarchy better?

✔ How can Futarchy be implemented in DAOs? Study of Meta-DAO.

✔ How can we participate in a Futarchical governance?

The Idea

If we were in an ideal world, we would have all the ‘perfect’ information needed to make a well-defined choice. Unfortunately, this is not a perfect world. We rather, can reach at least 99% towards it. If we aggregate all information needed to make well informed decision, the outcome will not just benefit us, but all. However, one always succumbs to greed, bureaucracy or personal benefits, when making such decisions. This is where democracy majorly fails. This type of governance is mostly used form in the world. We have 24 full democracies in the world and 48 flawed democracies. The institutions within democracy who make decisions for improving societal conditions, are extremely important to us.

Consider a time of elections (an example inspired from Hansen, 2007). Two opponents are running for President in Duckberg: Goofy and Donald Duck.

A group of voters in Duckberg, who are well-informed in a sense that, they have read the opinion polls, follow news, understands pros and cons of political agendas and macroeconomic factors, short and long term goals, vote for Goofy.

While majority perhaps, who favoured Donald duck based on the short lived promises and being less informed of opinions, news, agendas etc., vote for Donald Duck.

As an outcome, Donald Duck wins which hurts many voters who were quite well informed. As expected by them, the government elected, fails in coordination or to commit towards better interest of the nation. It could be that Duck is representing a government that is self-serving.

If all the voters had a high incentive to be informed, they would have then made an informed choice as well. In this case, voters would vote on information and values and bet on beliefs that the future government will work for the benefit of all.

There can be many examples of the conventional model of governance affected by less information, yellow and captured journalism leading to a poorly informed populace and political agendas. CEOs making decisions which is in their own interest/stakeholders rather than the whole company, government heads imposing policies based on personal vendetta against minor groups, a minister appointing his nephew as the governor of a national bank who does not have any experience in conducting monetary policies. We as humans tend to make many errors, with or without proper information and icing on top, we do not live in an ideal world!

An alternative solution to such form of governance would be using the speculative or prediction markets and letting them be the monarch. Speculative markets show very less information failure. One example of speculative market would be of stock markets. Huge financial literature can back the fact that stock markets run on the element of dealer’s beliefs and speculations of traders. ‘The market gives more weight on experts, both public and private’ - Hansen (2007). The market fundamentally, gives more importance to better predictors. We bet on future price of a stock, say - buying at a low price and expecting to sell at a higher price. The well-informed can speculate that ‘future price of this stock will definitely rise’, betting and consistently pushing the stock’s current price towards the speculated price.

Traders can also be much more informed than others, with no incentive of sharing that information with other participants (insider), which is major drawback. However, ideally the trader (insider) can share the information for the current price to be speculated accordingly, this will eliminate inefficiency of the markets. Such an ideal scenario never occurs, though. These markets also, sometimes, tend to not perform to their full potential due to many other economic imperfections such as, information asymmetry, government intervention, adverse selection, skewed judgements etc. Stock markets are one example of prediction market. It is a market mix of many strategies, a participant or an investor, can apply for protecting herself from risk, loss or creating more profit, such as short selling, hedging, long-short positions, even using derivative hedging etc..

But the idea from this market is of a special use. A prediction market has more information aggregation techniques, therefore, making it a viable candidate for efficient working of an economy or to be used as a novel governance model, decentralized or centralized. We will soon see how —

The Workings of Prediction Markets: Understanding the Basics

We find that market prices are far better predictors in the period without polls than when polls were available (Erikson & Wlezien, 2012). A prediction market, also named, "information markets," "idea futures" or "event futures", aggregates information through three main roles:

Incentive to seek more information

Incentive for ‘pulling truthful information out’ and

Aggregating diverse opinions.

These markets are usually binary in nature and are adopted for both centralized and decentralized platforms. As opposed to centralized, decentralized markets takes a higher stance considering low transaction fees, no jurisdictional requirements, offering fair, secure and transparent arena. A prediction market will set up two markets for one proposal. The process is based on conditional probability theorem: simply, given 2 beers, what is the expected outcome of being drunk? Is the expected outcome higher than ‘if the 2 beers were not given’. Let’s take a basic example —

Consider a beer company called ‘Pawtucket’ based in New York. The forecast in this market is set for: Will the price of beer reach an all-time high in 2024?

Yes, with a market price of $0.2 and,

No, with a market price of $0.8. - a much more likely outcome according to crowd consensus.

Now, let’s say Peter and Joe are two employees in Pawtucket who discuss about this forecast.

Peter thinks that the price of beer will reach an all-time high in 2024, selecting ‘Yes’ while Joe thinks otherwise, selecting ‘No’.

Peter then invests 50 USD for the outcome ‘Yes’, which means buying 250 shares ($50/$0.2) and Joe invests 100 USD (being confident enough) for the outcome ‘No’ buying 125 shares.

If the price of beer reaches an all-time high, Peter wins and collects 250 USD while Joe loses. If price of beer does not reach an all-time high, Joe wins with 125 USD while Peter loses.

‘Yes’ will be riskier bet than No but with higher return to investment. However, more than betting on a riskier outcome, it is about betting on well-informed outcome. If Peter would have invested 100 USD and if the outcome turned out in his favour, he would have collected 500 USD.

As more people make such trades, the market price stabilizes over the specified time, creating a close to an accurate forecast. A prediction market is utilised by the model of Futarchy in which future outcomes of interest (with some measure of welfare, say GDP) are bet on, conditional on certain policy being accepted/rejected. The markets have some time to settle on prices and then, ideally, prices conditional on the policy being accepted (or rejected) will be significantly different from prices conditional on the policy being rejected (or accepted). The market adjusts itself and corrects the mispricing.

In an efficient capital market, asset prices reflect all relevant information and thus provide the best prediction of future events given the current information.

-Paul Rhode and Koleman Strumpf, Historical Presidential Betting Markets

Let’s note down some gaps as well. These drawbacks only recently came to surface while they are quite logical problems.

The Wisdom of Crowds: Contrary to this drawback, collective intelligence plays a vital role in prediction market. The crowd becomes wiser if the intelligence is aggregated (see Bottazi & Giachini, 2016). Meaning, the information coming from an interaction of heterogenous group of agents, may it be complete or incomplete, collects all possible information needed to correct the prices in the market. Think about the opposite of an intelligent market. Lack of wisdom can cause a failure of a prediction market. For one, crowd’s information and answers can be wrong. Second, it can be due to poor social influence, where one agent exploits the information to get better predictions out of a market — creating a depreciating effect on information. This effect is backed by literature on prediction markets. Third, decision-makers may be reluctant to take risks, instead preferring to make decisions that prioritize immediate benefits (short-term outcomes).

Following the herd: We can experiment this drawback on prediction markets already existing in real life. I tried on ‘Manifold prediction market’ platform. It is quite easy to see that many people just follow the option that has higher votes or high probability of occurrence, which is quite a herding behaviour. Another herding behviour would be of ‘following an influenced opinion’. Elon Musk tweets and all follow the opinion, skewing speculation.

Manipulation and Biases: Wolfers and Zitzewitz (2006) suggest that manipulative behaviour in prediction market is usually short lived. But it does exist to some level. The efforts of manipulation are run down on by other participants improving the accuracy even more, the biases created by manipulators often are soon corrected by the unbiased. This is not a certain drawback but, since it does exist, it cannot go unnoticed.

The Futarchical Markets: Understanding the Mechanism

The concept of Futarchy was built to improve three models, mainly governance-related (corporate, agency and national, as Hansen suggests). Think about the government and inflation rates, for example. Conventionally, adopting a policy for decreasing inflation rate, always seems to be a good option for any welfare-increasing related outcome. We, as citizens believe that ‘Government is doing something for decreasing inflation rates’. “Nothing comes from doing nothing” - as William Shakespeare once said. Yes, something should be done. No, sometimes, not doing anything may save us from even more damage. The power of choosing a policy as a solution, is in the hands of centralized head, say a Prime Minister. What if the government implemented the policy but, it doesn’t work and inflation rates increased three times more? What if the power was rather in the hands of well-informed people like researchers, subject matter experts, normal citizens who when given power can have an incentive to be informed enough. This is where Futarchy model of governance emerges as an efficient one.

Since speculative markets do so well at a task that democracies have troubles with, it is tempting to try to improve democracy by making them rely more on speculative markets.

-Robin Hansen, ‘Shall we Vote on values, but Bet on beliefs?’

Futarchy works on the principle of prediction markets. Entrusting market with complete control, basically creates an atmosphere of accuracy in outcomes. Under Futarchy, a participant doesn’t just vote on whether a particular policy should be implemented, rather on a specific metric that fact-checks if the policy will work, if implemented! A metric is needed in this market to conduct a cost-benefit analysis of adopting or not adopting a policy. The prediction market then takes over. A policy is put out to approve or reject, markets are then formed which bet on a ‘metric’ such as Gini coefficient to measure inequality, GDP measure for richness, carbon emission reduction for environment sustainability and many more. In a Futarchy, if the policy is approved or rejected in an intention to increase welfare of the system and based on the metric predicted by the market, the rewards will be paid and losing bids will get reversed. The policy then becomes a law - the Base rule of Futarchy. The policy chosen is after-the-fact based outcome.

Inspired from Bitget article (referenced), the above example of GDP can be easily used for understanding a Futarchy. In this Futarchical market, the base value used would be US Dollars ($) and the success metric will be GDP in trillion US Dollars, after 10 years. The proposal is then defined, which in this case is ‘Will Ban on Imports of semi-conductors, increase the GDP after 10 years?’ or ‘If no ban, will increase GDP after 10 years’. Now, two markets are formed based on a conditional probability estimate. Given the ban of imports, will increase GDP would be one expected outcome and given that there will be no ban/status quo, will increase the GDP, as another expected outcome.

The expected outcome of accepting the proposal (Yes) is an average $26.4, meaning that GDP will increase to $26.4 trillion US Dollars after 10 years.

The expected outcome of rejecting the proposal (No) is an average $28.7, meaning GDP will increase to $28.7 trillion US Dollars after 10 years.

This suggests that market outcomes have advised not to adopt the proposal. The trades on banning the imports, are reversed and the winning market gets rewarded at maturity. While it is completely possible that the rejection of proposal might not turn fruitful as well, if the rejection does not work effectively as predicted to be. But it is still a reliable bet in a sense that it is not driven by personal gains of a representative, politics, coordination or commitment failures etc. Market participants in such market, have tendency to correct mispricing (Proph3t, META-DAO) and therefore, could at least be more reliable.

These examples can be rehearsed on corporations or any organization with a human decision-maker. A very used and common example is of ‘CEO being fired or retained’. Contrary to the conventional decision making practices of such organizations or governments, a Futarchical market runs via the market.

With blockchain technology, we see emergence of decentralized prediction markets, which could serve as a foundation for implementing Futarchy.

⚡ What’s on my mind?

Key areas where Futarchy could potentially be implemented or experimented with:

Decentralized Finance (DeFi): DeFi protocols can leverage prediction markets for price discovery, risks management, and governance.

Governance: Organizations could experiment with Futarchy-based governance models to determine protocol upgrades, resource allocation or policy changes.

Tokenized Assets: Blockchain-based markets for tokenized assets with Futarchy mechanisms can help in optimizing asset allocation, portfolio management, and investment strategies. Predictive markets can help investors gauge market sentiments and market informed decisions.

Supply Chain Management: As blockchain dives further into supply chain solutions, there could be potential prediction markets to forecast demand, monitor inventory levels and optimize logistics (conditional to the design and governance structure of the system).

One can say, well why just one proposal to make a choice on (after-the-fact) and not consider other proposals? A choice of which policy will work effectively, should not necessarily be binary. In reply to Andrew Gelman’s — ‘Questions about Futarchy’, Columbia University, Hansen suggests threshold of approval. Speculators can consider different proposals and cancel first proposal using combinatorial approaches.

⚡ What’s on my mind?

In addition to Robin Hansen’s reply, one can also think about ‘Forward Induction’ famously used in statistical regression models along with threshold of approvals, in considering different combination of proposals for implementation and finding which can work the best.

Although, it seems easy to showcase examples of implementing Futarchy in national governance model or corporations, surprisingly, it is a very untried upgrade of democracy in real world. However, it can be quite challenging to implement Futarchy in real-life, it is almost pioneering!

Criticisms of Futarchy:

While Hansen (2007) lists 33 different issues with Futarchy, many others also cite the issue with the concept of Futarchy. In addition to already-mentioned drawbacks of Prediction markets, limitations of Futarchy can be —

Lack of Vote Value Stage: Futarchy involves two stages: One, where prediction markets determine which decision is expected to bring out the best outcome. Followed by voting stage which is, accept or reject the decision. However, some proposals can skip the votes values stage, assuming that the metric optimized, is the price of the underlying token. This limits the types of decisions, Futarchical governance can effectively make. Incorporating "vote values" stage may introduce few more drawbacks like voter apathy, manipulation, or difficulty in reaching a consensus.

The Welfare Metric: Hanson stresses on ‘how to define the key metric’ for efficient decision making. Defining the metric independently from the policy process is very crucial to prevent improper influence by government representatives. However, there can be economic vs. social conflict, in terms of welfare. What are we trying to achieve?

Lack of Simplicity in Contract Structures: There is a need for simpler, more accessible and more aligned decision market mechanisms. Providing entire probability distributions, which can be complex and require significant expertise. Simplicity can encourage wider participation.

Public policy, however, cannot be devised with a simplistic process. It could potentially lead to bad decisions, leaving out important considerations.

Challenge of Unrewarded Advocacy: Individuals who support unlikely proposals, even if they believe strongly that the proposal might not work, may not see any reward if the proposal is not adopted. This can be a bit unfair.

Dilemma of Thin Markets: Thin markets are those where there is limited trading activity, therefore limited information, meaning there are relatively few buyers and sellers in the market. Therefore, in these markets a small amount of trading activity can have a significant impact on prices, making them potentially more susceptible to manipulation. A famous example would be of trading commodities like rare metals!

Long-term Forecast Decisions: It can be challenging to predict long-term outcomes or even to judge the accuracy of such an outcome, until closer to the event. Therefore, there can be slight uncertainty about whether the market predictions can be trusted for making policy decisions well in advance.

Hanson suggests waiting for a consistent price signal in the market before adopting a policy.

Institutional Costs: Evaluating proposals incur costs, necessitating a framework to limit new proposals. Hanson proposes a fee to consider proposals, potentially excluding those without significant financial resources from initiating policy changes. This could privilege the wealthy and special interest group in the proposal process, side-lining societal interests.

How to fix Bad Decisions? : Policies may contain bugs or over simplifications that require correction. The elected government should have the power to amend policies or the welfare function. However, the process may be slow and costly, and the influence of deep-pocketed interests could undermine the effectiveness of the appeal process.

Fact Testing of Forecast Accuracy: It is easy to test accuracy depending on after-the-fact metric, but comparing market forecast and outcome can be complex. The time lag in testing decision markets' accuracy could hinder meaningful evaluation Hanson compares them to horse race betting markets which oversimplifies the challenges of forecasting complex policy outcomes.

As mentioned very early in this article, this century has a unique opportunity to become pioneers in serving better to the world, leveraging Web 3.0 capabilities.

The concept of Futarchy can finally come to light in an entity with no central leadership: Decentralized Autonomous Organizations (DAOs).

A Brief on DAOs —

DAO short for, Decentralized Autonomous Organization is owned and operated by its community members. As the fundamental principle of Web 3.0, a DAO has no central head or is not a centralized organization — ensuring transparency, collaboration, equality and reliability. It is blockchain-based operation, the core function of which is to issue digital currency to members of a DAO, referred as governance tokens. This provides voting power for the holder of the token. Funds are stored in their own treasury and are governed by smart contracts on the blockchain. The rules encoded cannot be changed unless voted by DAO members. For moving the DAO forward with better decisions, the token holder vote for or against proposals.

Seems like the best stage for Futarchy to shine, doesn’t it? 😉

“The Meta-DAO is a new kind of organization” - Meta DAO Docs. The Meta-DAO has adopted Futarchy as their fundamental mechanism, making it an exceptionally unique form of experimental success in today’s world. Futarchy along with DAOs can counterbalance the spread of incorrect information, creating a financial incentive for truth and making better decisions for organizations.

The Meta-DAO

To solve the inefficiencies of a conventional democratic model of governance, Meta-DAO untangles the challenge of using Futarchy as their core principle of working. The ideology is - decision-making power must be in the hands of the market not human decision makers of institutions - and is based on the concept of innovation, equality, transparency, autonomy and sustainability. The Meta-DAO can be considered as the first use-case of implementing Futarchy in the organization. All Meta-DAO markets are on central-limit order-book program or a trading system that matches orders. The key players are the market and members within that market. These members are defined as ‘single-product profit-seeking entities’. With each having their own treasury, they can pay grants, payroll and suppliers from it. They have their own token, META, which is analogous to a share in a company.

These members are collectively called the Meta-DAO.

Meta DAO is a decentralized distributed autonomous organization, co-sponsored by Meta Virtual Reality Labs (Meta Reality Labs), a subsidiary of Meta, and Singapore GIC Capital, aiming to realize Web 3.0 by building the early infrastructure and ecology of Metaverse and Industrial integration development.

-Meta DAO docs

How does Meta-DAO do it and how can you participate?

The working of Futarchy is explained but how is it implemented in Meta-DAO? Retracing the steps of how Futarchy works and applying to how Meta-DAO works:

Connect your wallet - attain USDC and/or META

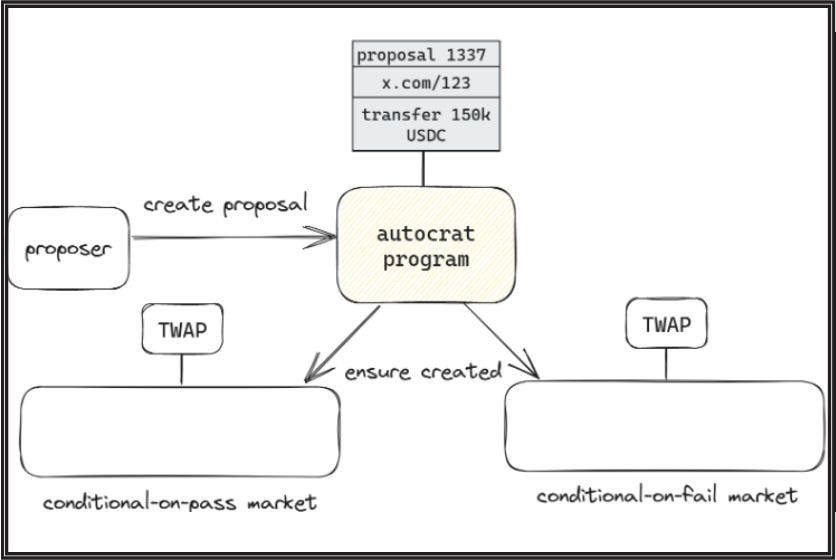

You/anyone can create proposal / question - For this, the organization is comprised of a program called ‘Autocrat’. Anyone can interact with Autocrat to create a proposal. A proposal creation consists of proposal description, an executable Solana Virtual Machine (SVM) instruction and proposal number. For example, Peter can create a proposal to transfer 200,000 USDC to a development team, creating an improvement proposal to improve a product that’s managed by the Meta-DAO. The idea of the proposal is to evaluate the value of the proposal and if it may or may not add value to the Meta-DAO. This creates conditional vaults and markets at the same time.

Note: The proposal creation first undergoes a discussion and then, is formulated into a draft (on Discord).

You need a success metric and base value: The base value in Meta-DAO is META or USDC. The success metric built by Meta-DAO themselves is ‘Time Weighted Average Price (TWAP)’. It is a pricing algorithm which is used to calculate the average price of an asset over a specified time period.

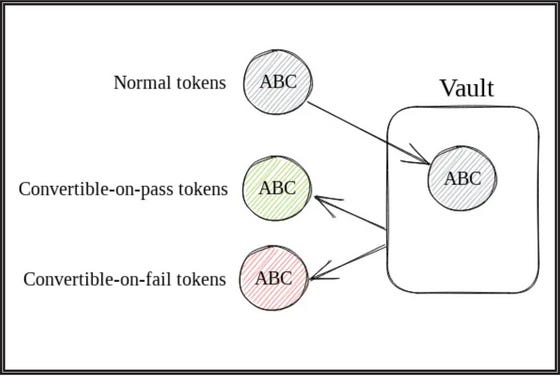

You need a vault, where you can deposit tokens. Two vaults are created by Meta-DAO, one for USDC and one for META, allowing the reverting process to happen. You can then exchange the underlying token, META or USDC for two types of conditional tokens to deposit in conditional vaults — which is a new primitive to carry out the implementation (A Meta-DAO Manifesto).

Conditional-on-finalize (Conditional-on-pass), which you can redeem if vault is finalized and,

Conditional-on-revert (Conditional-on-fail), you can redeem if vault is reverted.

For example, you deposit USDC, this will mint pUSDC and fUSDC. Similar with META. You can mint conditional-on-pass (pMETA) and trade it for conditional-on-pass (pUSDC). If the proposal passes, you can redeem pUSDC for USDC. If the proposal fails, you can redeem fMETA and trade it for fUSDC and redeem for USDC.

Market takes time (stated 5 days) and settlement authority which is Meta-DAO finalizes or reverts the proposal. If finalized, the success metric, TWAP is judged by the autocrat program. If the TWAP for pass market is higher than that of fail then, the SVM instruction is run — finalizing the pass market and reverting the fail market as an outcome. Assuming an efficient proposal, the price of META will be driven throughout the time period until finalisation - to give an accurate estimate of the expected value reflecting all available information — leading to an efficient market. [Efficient Market Hypothesis]

Orders: Altogether, you will be able to see the proposal pass or fail, along with vaults on the left of the screen. You can also see orders at the bottom as well that suggests if you wish to settle or cancel orders. You can also see the ‘uncranked’ orders where, ‘the cycle icon with the 12 on it next to the respective market will crank and push the orders into the Unsettled’. You can close and settle orders to re-claim SOL as well.

💥 Have a look at the 10th proposal in the app of Meta-DAO (click here) which at the time of writing this article, is still pending on outcome. Their interesting proposal on increasing Meta DAO's protocol-owned liquidity, should give an idea of how proposals are drafted for prediction in the Futarchical Meta-DAO. Past proposals as well, when clicked shows a format of how you can mint tokens and see the Pass and Fail of a particular proposal. This should be the starting point and a great way to begin participating.

⚡ What’s on my mind?

Let’s discuss Mechanism —

As discussed earlier, the Meta-DAO uses conditional vaults, markets and TWAP oracles to enable decision-making based on market prediction. I would like to compare the Meta-DAO mechanism to VCG (Vickrey-Clarke-Groves) mechanism, originally proposed by Yang Cai, Mohammad Mahdian, Aranyak Mehta and Bo Waggoner (2018).

VCG is a hybrid auction-prediction, offers a novel approach to decision-making by combining individuals’ preferences and predictions in a transparent and incentive-compatible manner. It allows participants to submit bids based on both their preferences and probabilistic forecasts, the mechanism aims to optimize outcomes while ensuring truthfulness and fairness. This mechanism holds promise applications in areas like network routing decisions, public project selection, procurement auction, where aggregating diverse perspectives and accurate predictions is crucial for achieving optimal results. However, challenges like budget imbalances and inefficient information aggregation remain to be addressed to extract the potential of this hybrid approach.

While both the mechanisms involve decision making, the core difference between these two mechanisms is that VCG can be applied in centralized or semi-centralized setting like government auctions, resource allocation in multi-agent systems (supply chain management), and spectrum auctions (licenses for 5G networks), while the Meta-DAO mechanism is used for decentralized governance within blockchain-based organizations.

Having more metrics than just one, can effectively pull out accurate outcomes. However, the challenge lies in the designing the system which can balance and prioritize these diverse metrics, especially when these metrics may conflict each other. A metric needs to carry the importance of each of the metrics and establish a trade-off.

One of the mentioned limitations for Meta-DAO in early stages is limited interest and low liquidity with it. Proph3t (creator of Meta-DAO) proposed few ideas like liquidity mining, NFTs for early adopters and incorporating a multisig with veto powers in early stages of governance. Other ideas that I have in mind are:

(1) Incentive Program for Market Analysis - rewarding participants for contributing market analysis that can enhance quality of information available in prediction markets. This could potentially align with the goal of accurate forecasting.

(2) Localized Community Initiatives - building specific communities around prediction markets can not only increase engagement but also has the potential to not depend on Schelling Point dependence.

Final Thoughts

Centralized implementation of Futarchy has many challenges and who knows how the dream implementation of this model of governance may turn out. The fear of running into the limitations of Futarchy, can hold many aback. Trial and error takes time but we can experiment in the space of Decentralized ecosystem, now that we have a chance. The long-term outlook of Futarchy on decentralized system, according to me, aligns with Vitalik Buterin (Founder of Ethereum) in a sense that DeFi protocols can adapt to Futarchy from day one. The Meta-DAO has endowed us with a great way to understand how Futarchy can play out and how we can use markets up to their complete potential.

I hope the future holds best for social welfare on national and international level, considering an extensive research still to be done. Cheers and thanks for reading my article on Futarchy - where the market is the king!

References:

Introduction

The Idea

The workings of Prediction Market: Understanding the Basics?

The Futarchical Market: Understanding the Mechanism

A brief on DAOs—

The Meta-DAO

How does Meta-DAO do it and how can you participate?

- help from Meta-DAO documents

The Meta-DAO app - figures and understanding

What is TWAP? - Chainlink

What’s on my mind?